Spatially Explicit Markov Methods

Author: Serge Rey sjsrey@gmail.com, Wei Kang weikang9009@gmail.com

Introduction

This notebook introduces Discrete Markov Chains (DMC) model and its two variants which explicitly incorporate spatial effects. We will demonstrate the usage of these methods by an empirical study for understanding regional income dynamics in the US. The dataset is the per capita incomes observed annually from 1929 to 2009 for the lower 48 US states.

Note that a full execution of this notebook requires pandas, matplotlib and light-weight geovisualization package pysal-splot.

Classic Markov

giddy.markov.Markov(self, class_ids, classes=None)We start with a look at a simple example of classic DMC methods implemented in PySAL-giddy. A Markov chain may be in one of $k$ different states/classes at any point in time. These states are exhaustive and mutually exclusive. If one had a time series of remote sensing images used to develop land use classifications, then the states could be defined as the specific land use classes and interest would center on the transitions in and out of different classes for each pixel.

For example, suppose there are 5 pixels, each of which takes on one of 3 states (a,b,c) at 3 consecutive periods:

import numpy as np

c = np.array([['b','a','c'],['c','c','a'],['c','b','c'],['a','a','b'],['a','b','c']])

So the first pixel was in state ‘b’ in period 1, state ‘a’ in period 2, and state ‘c’ in period 3. Each pixel's trajectory (row) owns Markov property, meaning that which state a pixel takes on today is only dependent on its immediate past.

Let's suppose that all the 5 pixels are governed by the same transition dynamics rule. That is, each trajectory is a realization of a Discrete Markov Chain process. We could pool all the 5 trajectories from which to estimate a transition probability matrix. To do that, we utlize the Markov class in giddy:

import giddy

m = giddy.markov.Markov(c)

In this way, we create a Markov instance - $m$. Its attribute $classes$ gives 3 unique classes these pixels can take on, which are 'a','b' and 'c'.

print(m.classes)

print(len(m.classes))

In addition to extracting the unique states as an attribute, our Markov instance will also have the attribute trnasitions which is a transition matrix counting the number of transitions from one state to another. Since there are 3 unique states, we will have a $(3,3)$ transtion matrix:

print(m.transitions)

The above transition matrix indicates that of the four pixels that began a transition interval in state ‘a’, 1 remained in that state, 2 transitioned to state ‘b’ and 1 transitioned to state ‘c’. Another attribute $p$ gives the transtion probability matrix which is the transition dynamics rule ubiquitous to all the 5 pixels across the 3 periods. The maximum likehood estimator for each element $p_{i,j}$ is shown below where $n_{i,j}$ is the number of transitions from state $i$ to state $j$ and $k$ is the number of states (here $k=3$):

$$\hat{p}_{i,j} = \frac{n_{i,j}}{\sum_{q=1}^k n_{i,q} }$$print(m.p)

This means that if any of the 5 pixels was in state 'c', the probability of staying at 'c' or transitioning to any other states ('a', 'b') in the next period is the same (0.333). If a pixel was in state 'b', there is a high possibility that it would take on state 'c' in the next period because $\hat{p}_{2,3}=0.667$.

m.steady_state # steady state distribution

This simple example illustrates the basic creation of a Markov instance, but the small sample size makes it unrealistic for the more advanced features of this approach. For a larger example, we will look at an application of Markov methods to understanding regional income dynamics in the US. Here we will load in data on per capita incomes observed annually from 1929 to 2010 for the lower 48 US states:

Regional income dynamics in the US

Firstly, we load in data on per capita incomes observed annually from 1929 to 2009 for the lower 48 US states. We use the example dataset in libpysal which was downloaded from US Bureau of Economic Analysis.

import libpysal

f = libpysal.io.open(libpysal.examples.get_path("usjoin.csv"))

pci = np.array([f.by_col[str(y)] for y in range(1929,2010)])

print(pci.shape)

The first row of the array is the per capita incomes for the 48 US states for the year 1929:

print(pci[0, :])

In order to apply the classic Markov approach to this series, we first have to discretize the distribution by defining our classes. There are many ways to do this including quantiles classification scheme, equal interval classification scheme, Fisher Jenks classification scheme, etc. For a list of classification methods, please refer to the pysal package mapclassify.

Here we will use the quintiles for each annual income distribution to define the classes. It should be noted that using quintiles for the pooled income distribution to define the classes will result in a different interpretation of the income dynamics. Quintiles for each annual income distribution (the former) will reveal more of relative income dynamics while those for the pooled income distribution (the latter) will provide insights in absolute dynamics.

import matplotlib.pyplot as plt

%matplotlib inline

years = range(1929,2010)

names = np.array(f.by_col("Name"))

order1929 = np.argsort(pci[0,:])

order2009 = np.argsort(pci[-1,:])

names1929 = names[order1929[::-1]]

names2009 = names[order2009[::-1]]

first_last = np.vstack((names1929,names2009))

from pylab import rcParams

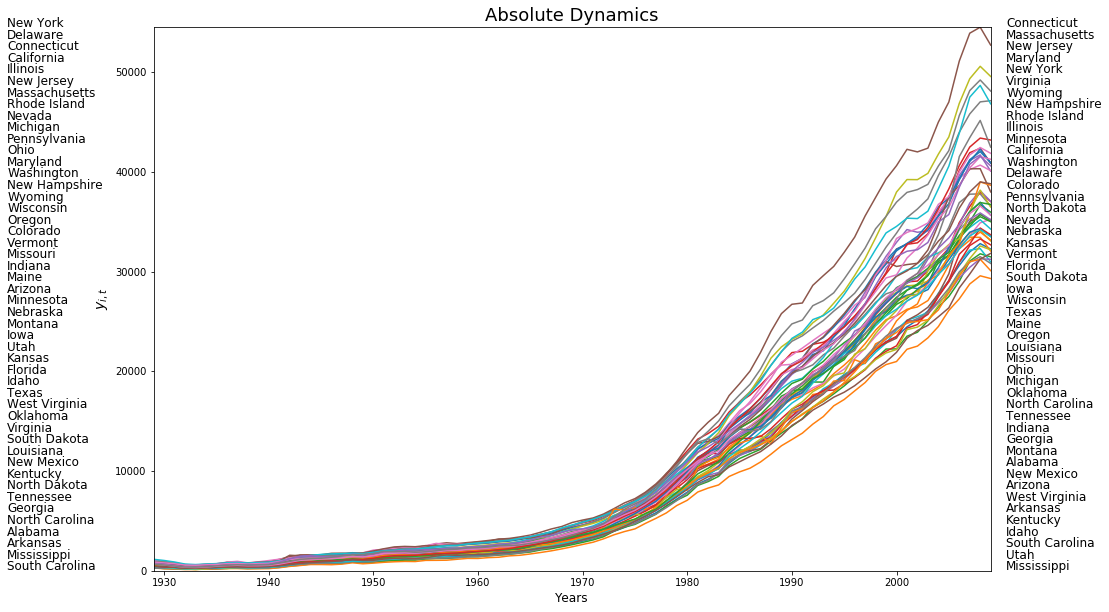

rcParams['figure.figsize'] = 15,10

plt.plot(years,pci)

for i in range(48):

plt.text(1915,54530-(i*1159), first_last[0][i],fontsize=12)

plt.text(2010.5,54530-(i*1159), first_last[1][i],fontsize=12)

plt.xlim((years[0], years[-1]))

plt.ylim((0, 54530))

plt.ylabel(r"$y_{i,t}$",fontsize=14)

plt.xlabel('Years',fontsize=12)

plt.title('Absolute Dynamics',fontsize=18)

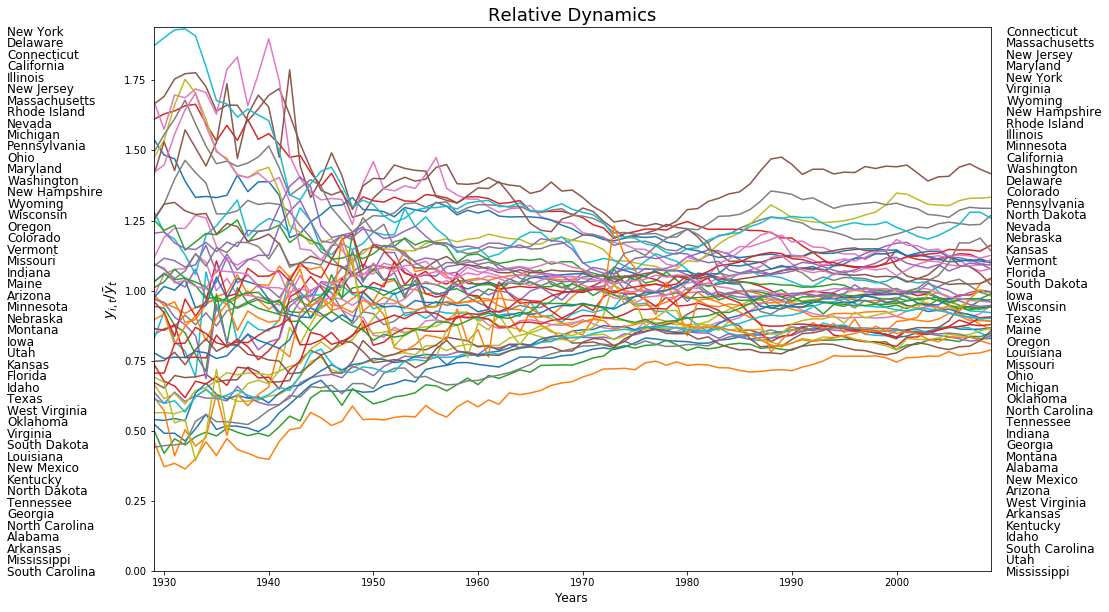

years = range(1929,2010)

rpci= (pci.T / pci.mean(axis=1)).T

names = np.array(f.by_col("Name"))

order1929 = np.argsort(rpci[0,:])

order2009 = np.argsort(rpci[-1,:])

names1929 = names[order1929[::-1]]

names2009 = names[order2009[::-1]]

first_last = np.vstack((names1929,names2009))

from pylab import rcParams

rcParams['figure.figsize'] = 15,10

plt.plot(years,rpci)

for i in range(48):

plt.text(1915,1.91-(i*0.041), first_last[0][i],fontsize=12)

plt.text(2010.5,1.91-(i*0.041), first_last[1][i],fontsize=12)

plt.xlim((years[0], years[-1]))

plt.ylim((0, 1.94))

plt.ylabel(r"$y_{i,t}/\bar{y}_t$",fontsize=14)

plt.xlabel('Years',fontsize=12)

plt.title('Relative Dynamics',fontsize=18)

import mapclassify as mc

q5 = np.array([mc.Quantiles(y,k=5).yb for y in pci]).transpose()

print(q5[:, 0])

print(f.by_col("Name"))

A number of things need to be noted here. First, we are relying on the classification methods in mapclassify for defining our quintiles. The class Quantiles uses quintiles ($k=5$) as the default and will create an instance of this class that has multiple attributes, the one we are extracting in the first line is $yb$ - the class id for each observation. The second thing to note is the transpose operator which gets our resulting array $q5$ in the proper structure required for use of Markov. Thus we see that the first spatial unit (Alabama with an income of 323) fell in the first quintile in 1929, while the last unit (Wyoming with an income of 675) fell in the fourth quintile.

So now we have a time series for each state of its quintile membership. For example, Colorado’s quintile time series is:

print(q5[4, :])

indicating that it has occupied the 3rd, 4th and 5th quintiles in the distribution at the first 3 periods. To summarize the transition dynamics for all units, we instantiate a Markov object:

m5 = giddy.markov.Markov(q5)

The number of transitions between any two quintile classes could be counted:

print(m5.transitions)

By assuming the first-order Markov property, time homogeneity, spatial homogeneity and spatial independence, a transition probability matrix could be estimated which holds for all the 48 US states across 1929-2010:

print(m5.p)

The fact that each of the 5 diagonal elements is larger than $0.78$ indicates a high stability of US regional income dynamics system.

Another very important feature of DMC model is the steady state distribution $\pi$ (also called limiting distribution) defined as $\pi p = \pi$. The attribute $steady\_state$ gives $\pi$ as follows:

print(m5.steady_state)

If the distribution at $t$ is a steady state distribution as shown above, then any distribution afterwards is the same distribution.

With the transition probability matrix in hand, we can estimate the first mean passage time which is the average number of steps to go from a state/class to another state for the first time:

print(giddy.ergodic.fmpt(m5.p))

Thus, for a state with income in the first quintile, it takes on average 11.5 years for it to first enter the second quintile, 29.6 to get to the third quintile, 53.4 years to enter the fourth, and 103.6 years to reach the richest quintile.

Thus far we have treated all the spatial units as independent to estimate the transition probabilities. This hides an implicit assumption: the movement of a spatial unit in the income distribution is independent of the movement of its neighbors or the position of the neighbors in the distribution. But what if spatial context matters??

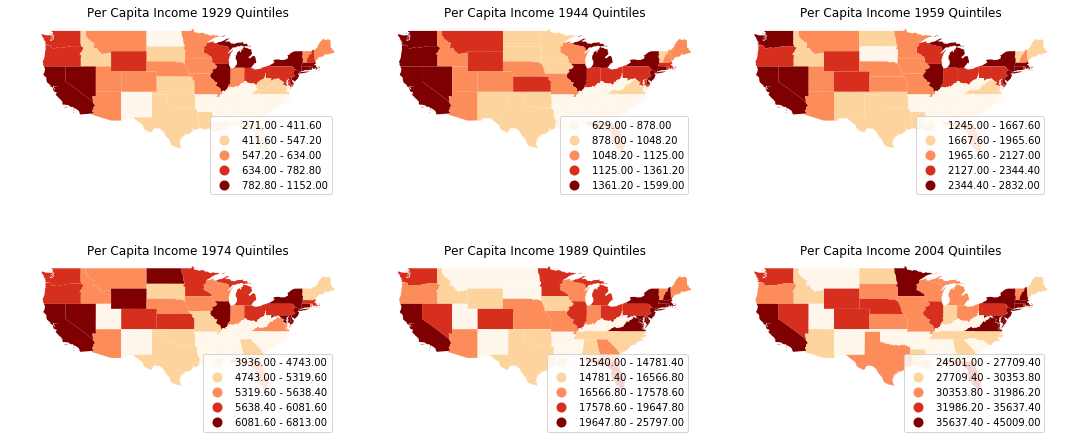

We could plot the choropleth maps of per capita incomes of US states to get a first impression of the spatial distribution.

import geopandas as gpd

import pandas as pd

geo_table = gpd.read_file(libpysal.examples.get_path('us48.shp'))

income_table = pd.read_csv(libpysal.examples.get_path("usjoin.csv"))

complete_table = geo_table.merge(income_table,left_on='STATE_NAME',right_on='Name')

complete_table.head()

index_year = range(1929,2010,15)

fig, axes = plt.subplots(nrows=2, ncols=3,figsize = (15,7))

for i in range(2):

for j in range(3):

ax = axes[i,j]

complete_table.plot(ax=ax, column=str(index_year[i*3+j]), cmap='OrRd', scheme='quantiles', legend=True)

ax.set_title('Per Capita Income %s Quintiles'%str(index_year[i*3+j]))

ax.axis('off')

leg = ax.get_legend()

leg.set_bbox_to_anchor((0.8, 0.15, 0.16, 0.2))

plt.tight_layout()

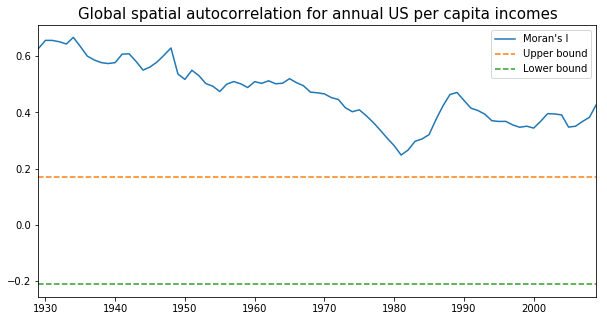

It is quite obvious that the per capita incomes are not randomly distributed: we could spot clusters in the mid-south, south-east and north-east. Let's proceed to calculate Moran's I, a widely used measure of global spatial autocorrelation, to aid the visual interpretation.

from esda.moran import Moran

import matplotlib.pyplot as plt

%matplotlib inline

w = libpysal.io.open(libpysal.examples.get_path("states48.gal")).read()

w.transform = 'R'

mits = [Moran(cs, w) for cs in pci]

res = np.array([(mi.I, mi.EI, mi.seI_norm, mi.sim[974]) for mi in mits])

years = np.arange(1929,2010)

fig, ax = plt.subplots(nrows=1, ncols=1,figsize = (10,5) )

ax.plot(years, res[:,0], label='Moran\'s I')

#plot(years, res[:,1], label='E[I]')

ax.plot(years, res[:,1]+1.96*res[:,2], label='Upper bound',linestyle='dashed')

ax.plot(years, res[:,1]-1.96*res[:,2], label='Lower bound',linestyle='dashed')

ax.set_title("Global spatial autocorrelation for annual US per capita incomes",fontdict={'fontsize':15})

ax.set_xlim([1929,2009])

ax.legend()

From the above figure we could observe that Moran's I value was always positive and significant for each year across 1929-2009. In other words, US regional income series are not independent of each other and regional context could be important in shaping the regional income dynamics. However, the classic Markov approach is silent on this issue. We turn to the spatially explict Markov methods - Spatial Markov and LISA Markov - for an explicit incorporation of space in understanding US regional income distribution dynamics.

Spatial Markov

giddy.markov.Spatial_Markov(y, w, k=4, m=4, permutations=0, fixed=True, discrete=False, cutoffs=None, lag_cutoffs=None, variable_name=None)Spatial Markov is an extension to class Markov allowing for a more comprehensive analysis of the spatial dimensions of the transitional dynamics (Rey, 2001). Here, whether the transition probabilities are dependent on regional context is investigated and quantified. Rather than estimating one transition probability matrix, spatial Markov requires estimation of $k$ transition probability matrices, each of which is conditional on the regional context at the preceding period. The regional context is usually formalized by spatial lag - the weighted average income level of neighbors:

$$z_{r,t} = \sum_{s=1}^{n} w_{r,s} y_{s,t}$$where $W$ is the spatial weight matrix and $w_{r,s}$ represents the weight that spatial unit $s$ contributes to the local context of spatial unit $r$ at time period $t$.

Similar to the construction of a Markov instance, we could create a Spatial Markov instance by utilizing the $Spatial\_Markov$ class in giddy. The only difference between the adoption of $Markov$ and $Spatial\_Markov$ class is that the latter accepts the original continuous income data while the former requires a pre-classification/discretization. In other words, here we do not need to apply the classification methods in mapclassify as we did earlier. In fact, the Spatial Markov class nested the quantile classification methods and all we need to do is set the desired number of classes $k$ when creating the $Spatial\_Markov$ instance. Here, we set $k=5$ (quintile classes) as before.

Different from before, quintiles are defined for the pooled relative incomes (by standardizing by each period by the mean). This is achieved by setting the parameter $fixed$ as True.

giddy.markov.Spatial_Markov?

sm = giddy.markov.Spatial_Markov(rpci.T, w, fixed = True, k = 5,m=5) # spatial_markov instance o

We can next examine the global transition probability matrix for relative incomes.

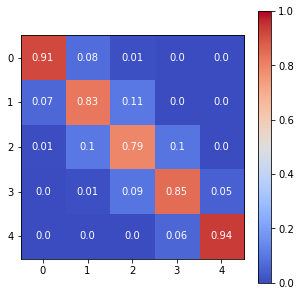

print(sm.p)

The Spatial Markov allows us to compare the global transition dynamics to those conditioned on regional context. More specifically, the transition dynamics are split across economies who have spatial lags in different quintiles at the preceding year. In our example we have 5 classes, so 5 different conditioned transition probability matrices are estimated - P(LAG0), P(LAG1), P(LAG2), P(LAG3), and P(LAG4).

sm.summary()

fig, ax = plt.subplots(figsize = (5,5))

im = ax.imshow(sm.p,cmap = "coolwarm",vmin=0, vmax=1)

# Loop over data dimensions and create text annotations.

for i in range(len(sm.p)):

for j in range(len(sm.p)):

text = ax.text(j, i, round(sm.p[i, j], 2),

ha="center", va="center", color="w")

ax.figure.colorbar(im, ax=ax)

fig, axes = plt.subplots(2,3,figsize = (15,10))

for i in range(2):

for j in range(3):

ax = axes[i,j]

if i==1 and j==2:

ax.axis('off')

continue

# Loop over data dimensions and create text annotations.

p_temp = sm.P[i*3+j]

for x in range(len(p_temp)):

for y in range(len(p_temp)):

text = ax.text(y, x, round(p_temp[x, y], 2),

ha="center", va="center", color="w")

im = ax.imshow(p_temp,cmap = "coolwarm",vmin=0, vmax=1)

ax.set_title("Spatial Lag %d"%(i*3+j),fontsize=18)

fig.subplots_adjust(right=0.92)

cbar_ax = fig.add_axes([0.95, 0.228, 0.01, 0.5])

fig.colorbar(im, cax=cbar_ax)

fig, axes = plt.subplots(2,3,figsize = (15,10))

for i in range(2):

for j in range(3):

ax = axes[i,j]

if i==0 and j==0:

p_temp = sm.p

im = ax.imshow(p_temp,cmap = "coolwarm",vmin=0, vmax=1)

ax.set_title("Pooled",fontsize=18)

else:

p_temp = sm.P[i*3+j-1]

im = ax.imshow(p_temp,cmap = "coolwarm",vmin=0, vmax=1)

ax.set_title("Spatial Lag %d"%(i*3+j),fontsize=18)

for x in range(len(p_temp)):

for y in range(len(p_temp)):

text = ax.text(y, x, round(p_temp[x, y], 2),

ha="center", va="center", color="w")

fig.subplots_adjust(right=0.92)

cbar_ax = fig.add_axes([0.95, 0.228, 0.01, 0.5])

fig.colorbar(im, cax=cbar_ax)

#fig.savefig('spatial_markov_us.png', dpi = 300)

The probability of a poor state remaining poor is 0.963 if their neighbors are in the 1st quintile and 0.798 if their neighbors are in the 2nd quintile. The probability of a rich economy remaining rich is 0.977 if their neighbors are in the 5th quintile, but if their neighbors are in the 4th quintile this drops to 0.903.

We can also explore the different steady state distributions implied by these different transition probabilities:

print(sm.S)

The long run distribution for states with poor (rich) neighbors has 0.435 (0.018) of the values in the first quintile, 0.263 (0.200) in the second quintile, 0.204 (0.190) in the third, 0.0684 (0.255) in the fourth and 0.029 (0.337) in the fifth quintile. And, finally the spatially conditional first mean passage times:

print(sm.F)

States in the first income quintile with neighbors in the first quintile return to the first quintile after 2.298 years, after leaving the first quintile. They enter the fourth quintile 80.810 years after leaving the first quintile, on average. Poor states within neighbors in the fourth quintile return to the first quintile, on average, after 12.88 years, and would enter the fourth quintile after 28.473 years.

Tests for this conditional type of spatial dependence include Likelihood Ratio (LR) test and $\chi^2$ test (Bickenbach and Bode, 2003) as well as a test based on information theory (Kullback et al., 1962). For the first two tests, we could proceed as follows to acquire their statistics, DOF and p-value.

giddy.markov.Homogeneity_Results(sm.T).summary()

From the above summary table, we can observe that the observed LR test statistic is 170.659 and the observed $\chi^2$ test statistic is 200.624. Their p-values are 0.000, which leads to the rejection of the null hypothesis of conditional spatial independence.

For the last (information theory-based) test, we call the function $kullback$. The result is consistent with LR and $\chi^2$ tests. As shown below, the observed test statistic is 230.03 and its p-value is 2.22e-16, leading to the rejection of the null.

print(giddy.markov.kullback(sm.T))

LISA Markov

giddy.markov.LISA_Markov(self, y, w, permutations=0, significance_level=0.05, geoda_quads=False)The Spatial Markov conditions the transitions on the value of the spatial lag for an observation at the beginning of the transition period. An alternative approach to spatial dynamics is to consider the joint transitions of an observation and its spatial lag in the distribution. By exploiting the form of the static LISA and embedding it in a dynamic context we develop the LISA Markov in which the states of the chain are defined as the four quadrants in the Moran scatter plot, namely, HH(=1), LH(=2), LL(=3), HL(=4). Continuing on with our US example, the LISA transitions are:

lm = giddy.markov.LISA_Markov(pci.T, w)

print(lm.classes)

The LISA transitions are:

print(lm.transitions)

and the estimated transition probability matrix is:

print(lm.p)

The diagonal elements indicate the staying probabilities and we see that there is greater mobility for observations in quadrants 2 (LH) and 4 (HL) than 1 (HH) and 3 (LL).

The implied long run steady state distribution of the chain is:

print(lm.steady_state)

again reflecting the dominance of quadrants 1 and 3 (positive autocorrelation). The first mean passage time for the LISAs is:

print(giddy.ergodic.fmpt(lm.p))

To test for dependence between the dynamics of the region and its neighbors, we turn to $\chi^2$ test of independence. Here, the $\chi^2$ statistic, its p-value and degrees of freedom can be obtained from the attribute $chi\_2$. As the p-value is 0.0, the null of independence is clearly rejected.

print(lm.chi_2)

References

- Rey, S. J. 2001. “Spatial Empirics for Economic Growth and Convergence.” Geographical Analysis 33 (3). Wiley Online Library: 195–214.

- Bickenbach, F., and E. Bode. 2003. “Evaluating the Markov Property in Studies of Economic Convergence.” International Regional Science Review 26 (3): 363–92.

- Kullback, S., M. Kupperman, and H. H. Ku. 1962. “Tests for Contingency Tables and Markov Chains.” Technometrics: A Journal of Statistics for the Physical, Chemical, and Engineering Sciences 4 (4). JSTOR: 573–608.